Model portfolio exposure allows you to identify the distribution of your investments across asset classes, equity sectors & industries, countries, regions, fixed income sectors, and more. Monitoring your portfolio's exposure relative to a benchmark helps ensure deviations are strategic.

Additionally, the Holdings Contribution table allows you to view which holdings make up your portfolio's exposure.

Model Portfolios functionality is available in the Advisor Core and Advisor Pro plans.

Exhibits

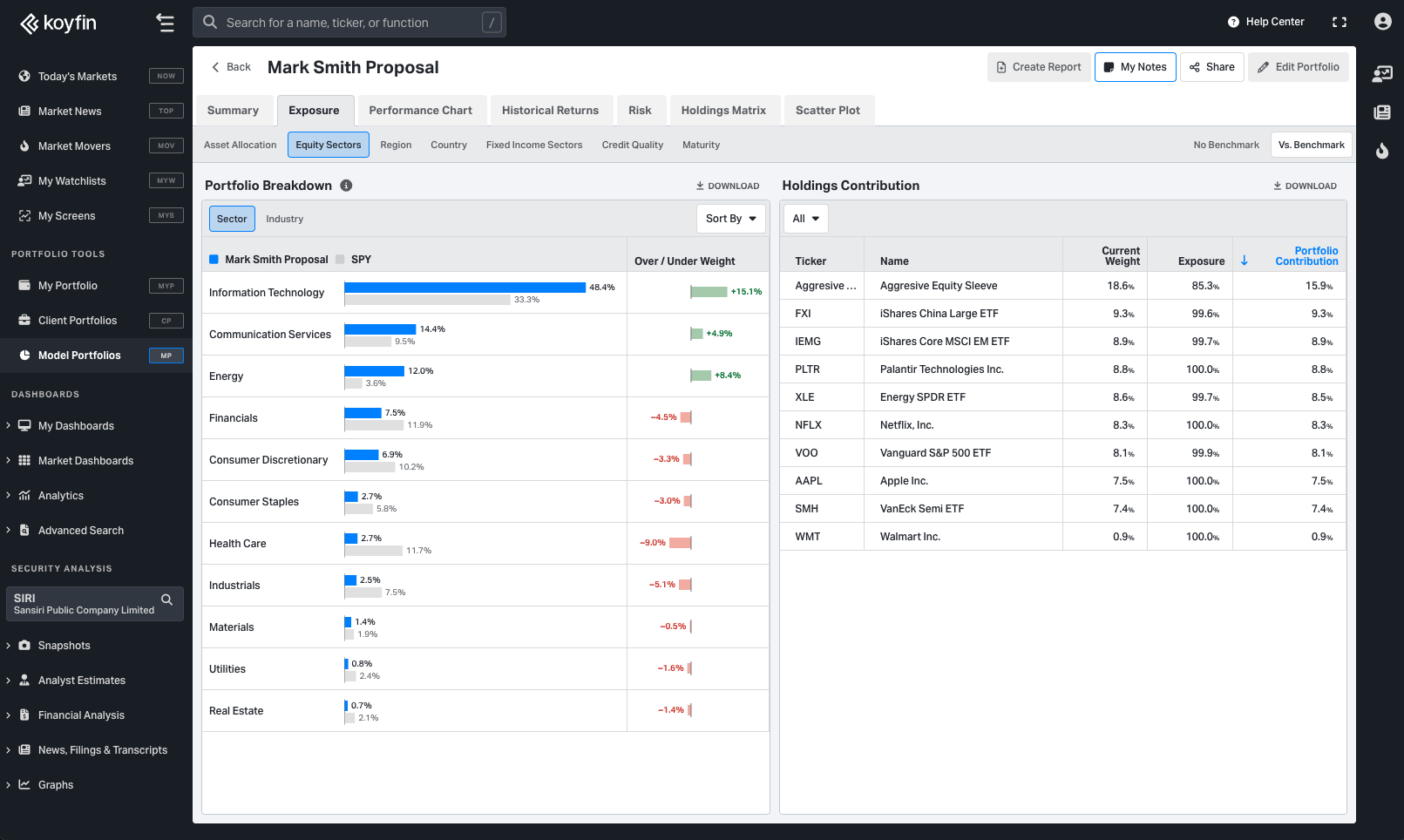

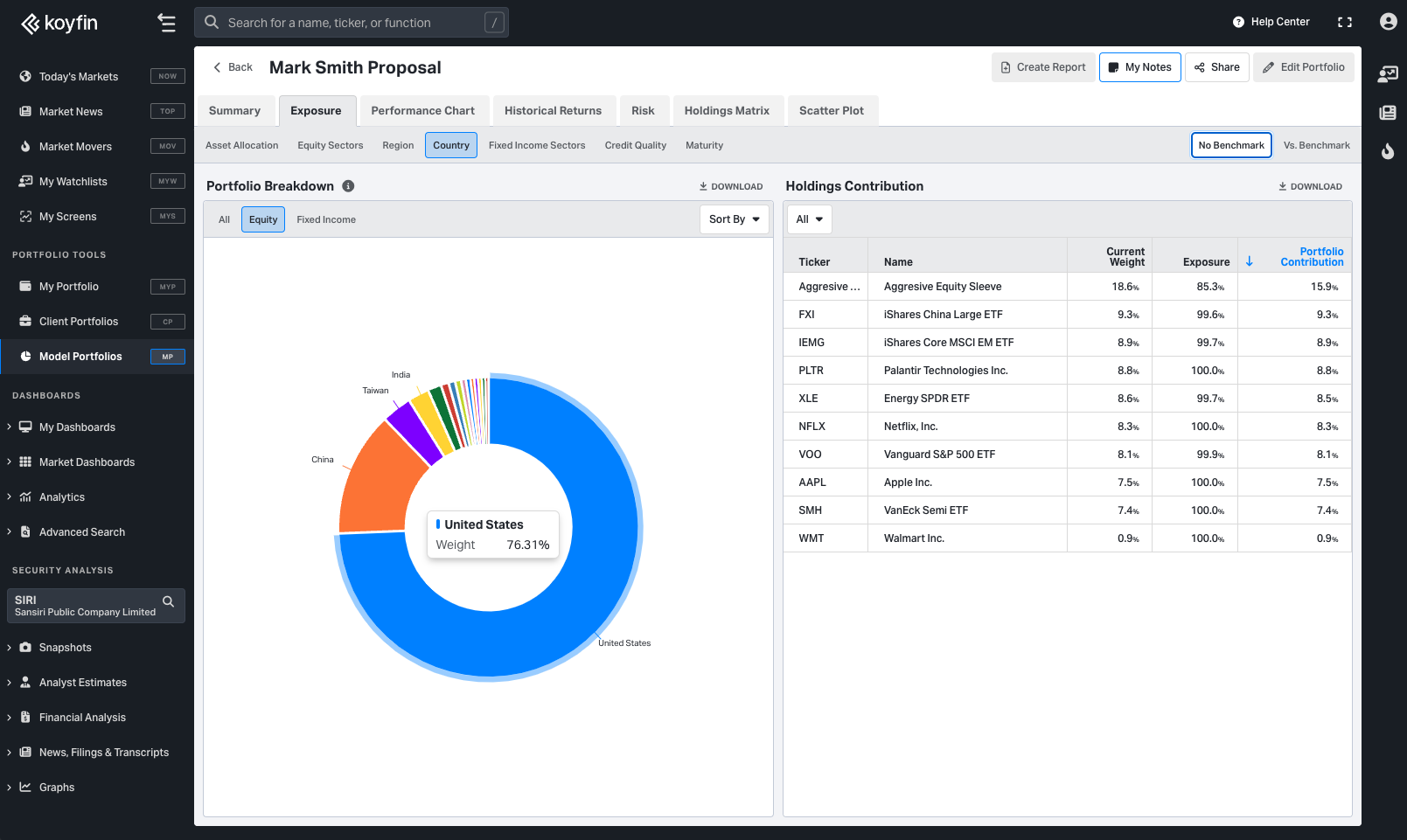

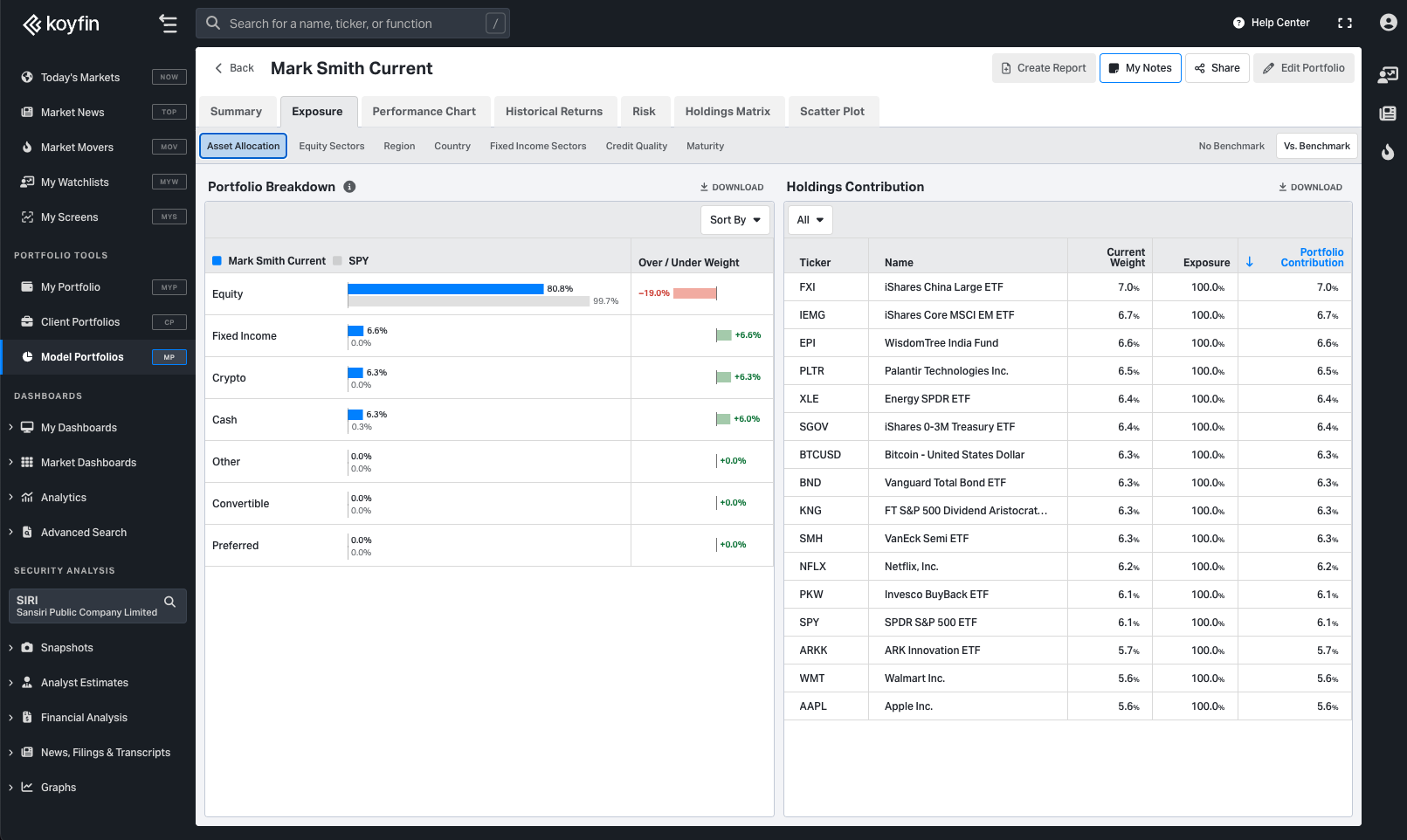

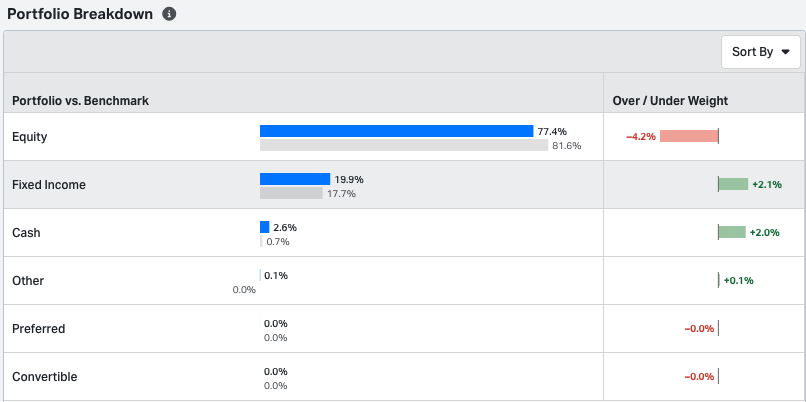

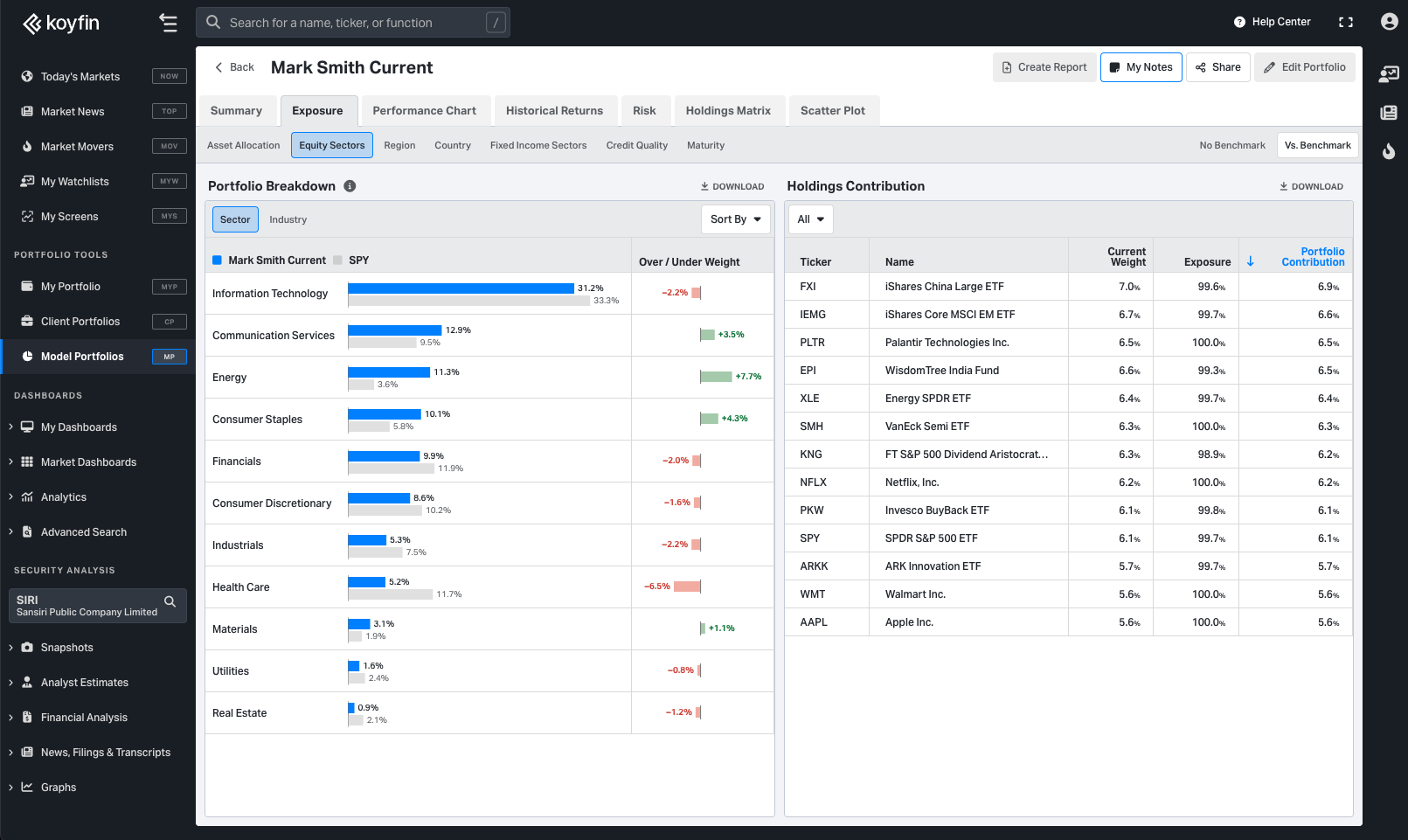

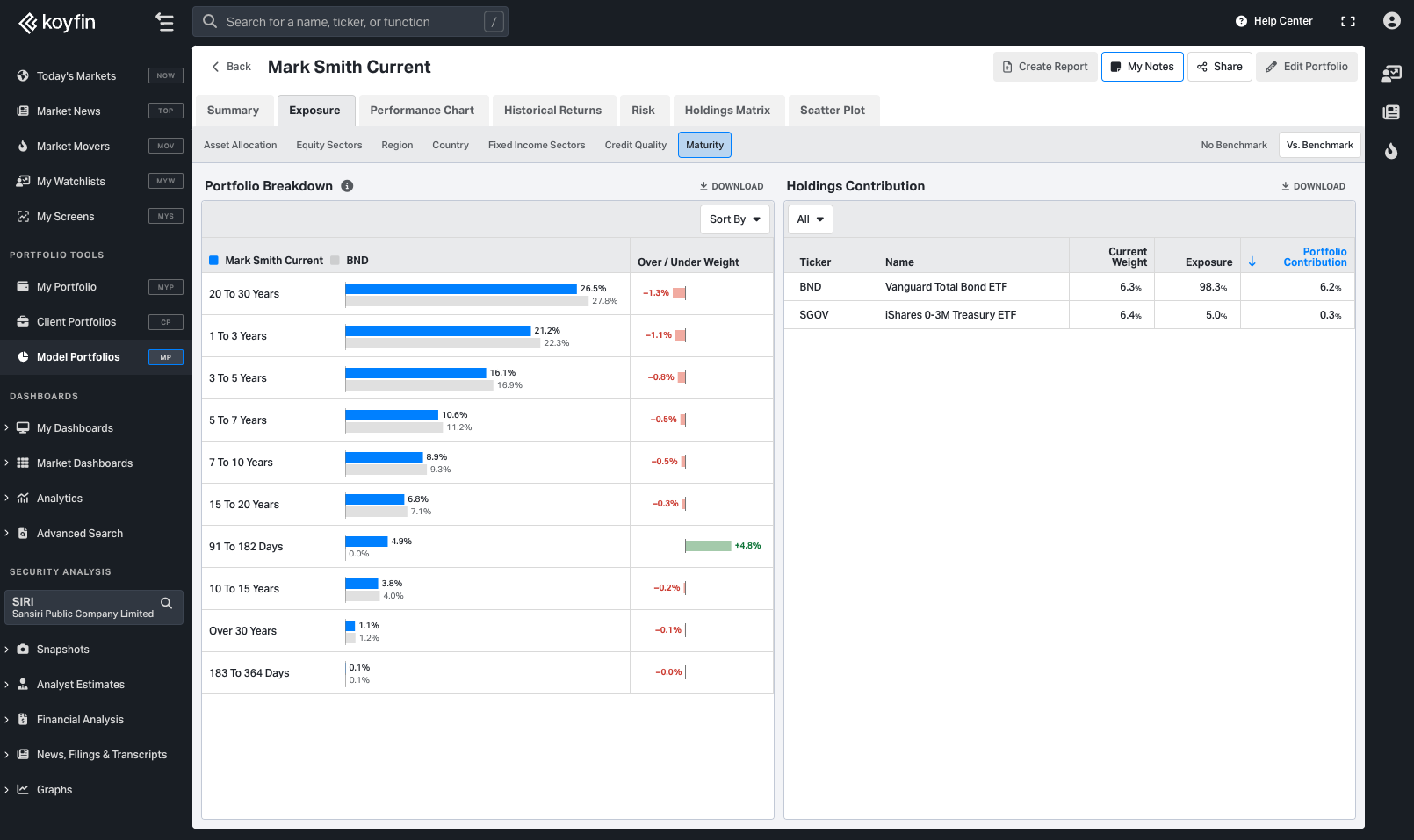

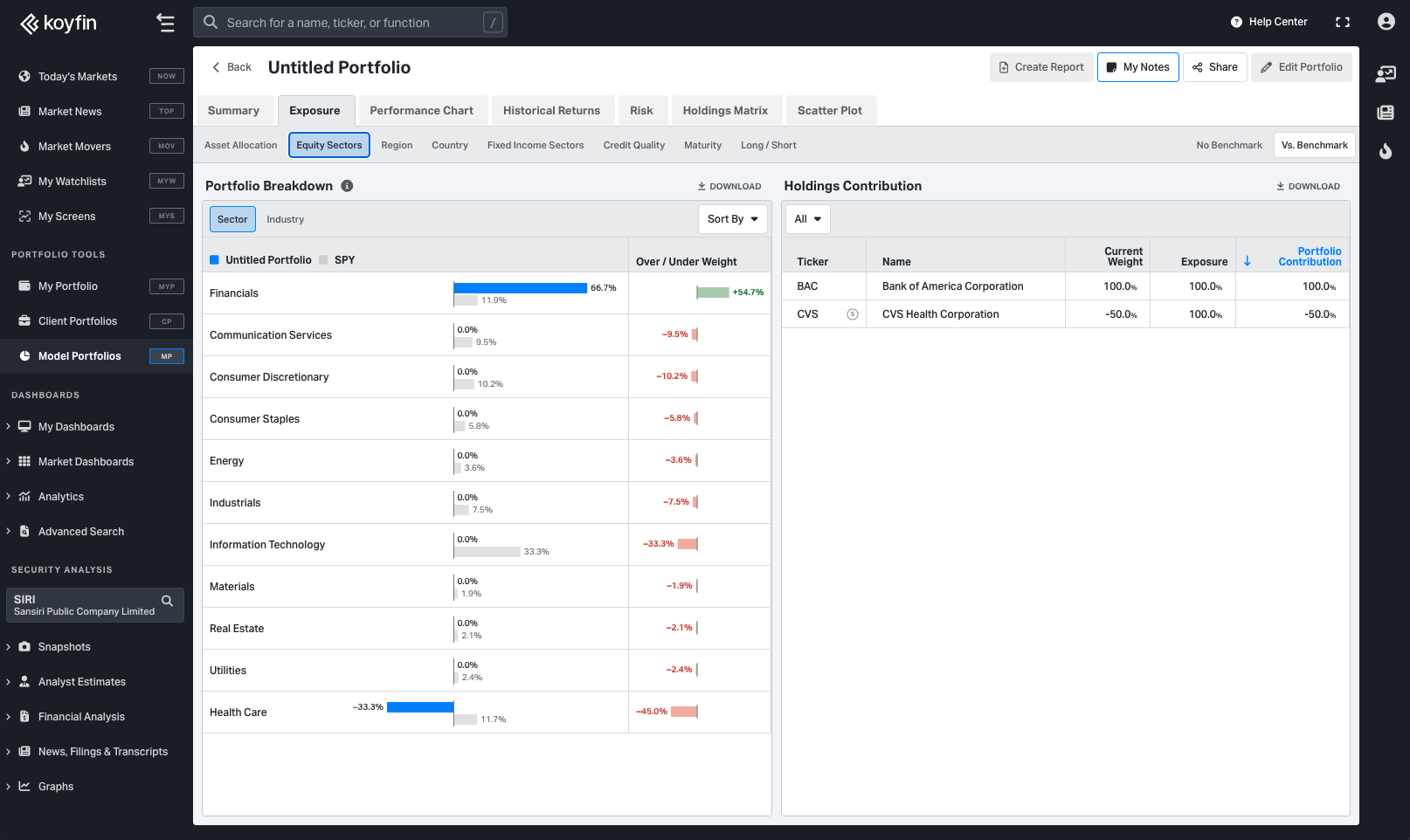

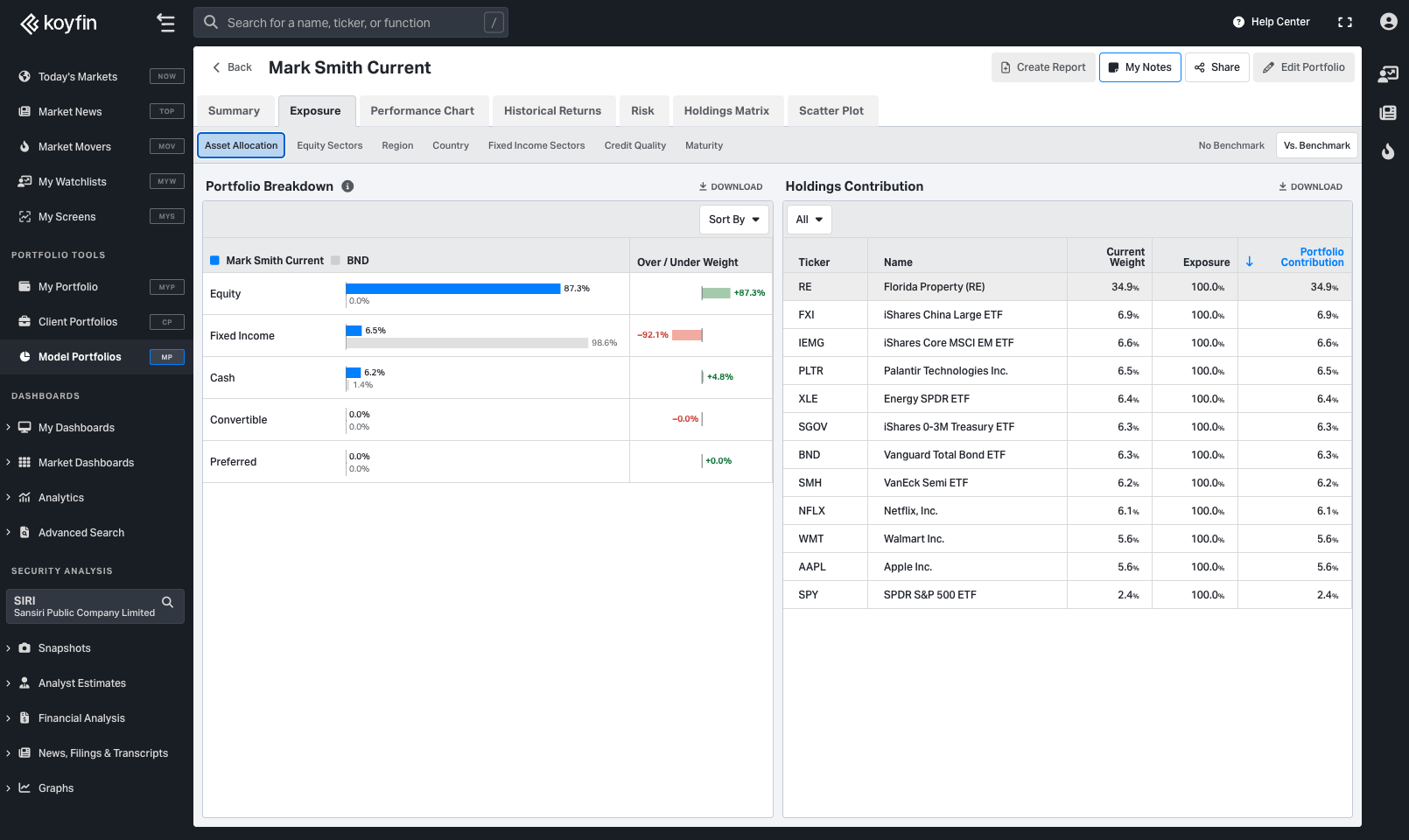

Navigate to the 'Exposure' tab to view your Model Portfolio broken out by Asset Allocation, Equity Sector & Industry, Region, Country, Fixed Income Sector, Fixed Income Credit Quality, or Fixed Income Maturity.

The 'No Benchmark' / 'Vs. Benchmark' toggle allows you to view the exposures as a pie chart (No Benchmark) or bar chart (Vs. Benchmark).

Asset Allocation

Monitor the mix of asset classes (such as equity, fixed income, and cash) within your portfolio.

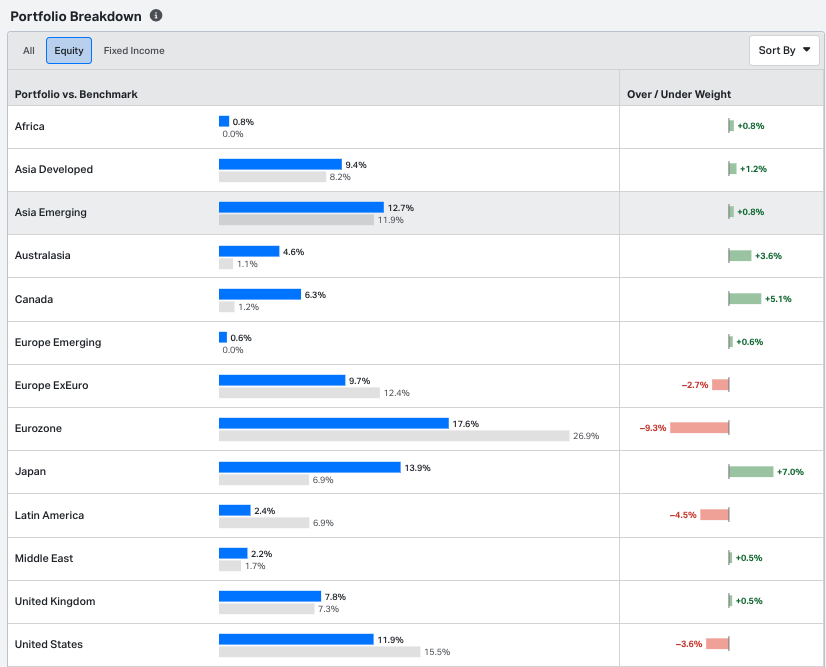

Geographic Breakdowns

Regional breakdowns provide insights into your portfolio's exposure to different regions and countries. We separate regional breakdowns into Equity, Fixed Income, and All. Cash allocations are exempt from this breakdown.

Equity Sector & Industry Breakdowns

Sector and industry breakdowns offer a closer look at your portfolio's distribution across equity sectors and industries. Cash allocations are exempt from this breakdown.

Fixed Income Exposures

For portfolios containing fixed income exposure, the Fixed Income Sectors, Credit Quality, and Maturity breakdowns will highlight those exposures in detail. Cash allocations are exempt from this breakdown.

Higher-rated bonds (e.g., AAA) are considered safer, while lower-rated bonds (e.g., B) can offer higher yields but come with greater risk. Bond maturity relates to the length of time until the bond's principal is repaid. Longer maturities usually offer higher yields but are more sensitive to interest rate changes. Cash allocations are exempt from this breakdown.

Holdings Contribution

Holdings Contribution allows you to drill down into specific exposures. For example: the Equity Sectors Holding Contribution allows you to see which holdings contribute to portfolio Technology or Healthcare exposure. See the below table listing each holding within a chosen category. For each holding, we have its:

- Portfolio Weight: Weight in the model portfolio

- Exposure: Percentage exposure to the selected sector, region, etc. (e.g., 50% of QQQ is invested in Information Technology stocks)

- Portfolio Contribution: Distributes 50% portfolio Information Technology exposure into 25% QQQ, 15% AAPL, 10% XLK

This granularity allows you to view outsized or underrepresented exposures, dive into the root cause, and modify your target weights accordingly to improve your model portfolio.

Custom Sorting

You can sort the Portfolio Breakdown chart by:

Portfolio Exposure: Order from largest to smallest to identify your top exposures by sector or region.

Over/Under Weight: Highlight sectors or regions with the most significant deviation from the benchmark.

Name (Alphabetical): Alphabetize country and industry names for easier location of specific exposures.

Coverage

Portfolio holdings are analyzed when they consist of global stocks, or ETFs, and Mutual Funds located in the U.S. or Canada.

However, ETFs domiciled outside the U.S. and Canada are only shown in the Holdings exhibit located on the Summary tab.

• For example, the UK-listed S&P 500 ETF, VUSA, will appear as a holding and be included in the performance of the model, but will not appear in the exposure tab exhibits.

Long-Only Exposures

For long-only portfolios, exposure exhibits will add to 100%. Breakdowns like Equity Sectors and Fixed Income Credit Quality will show the percentage of exposure within portfolio positions that have Equity or Fixed Income holdings. For example, in a 60% SPY (equity) and 40% TLT (bond) portfolio, the equity sector analysis will only reflect SPY.

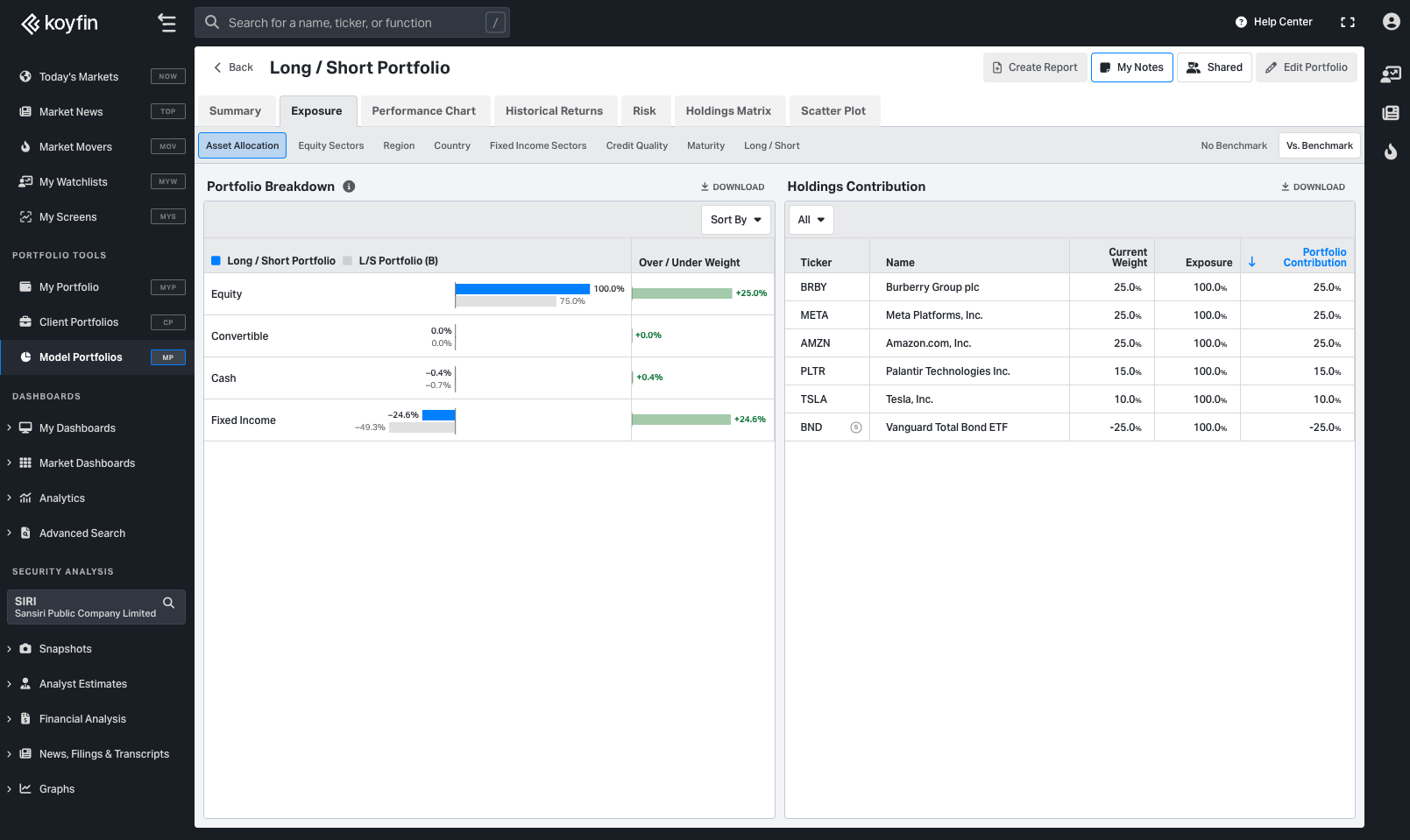

Long / Short and Leveraged Exposures

For Long/Short and/or Leveraged portfolios, exposures will be presented only as a bar chart format.

For the Asset Allocation, Holdings, and Region (All) and Country (All) exposures, the data will be presented as a net value relative to the gross portfolio exposure.

For example, this Long (100%) / Short (25%) portfolio is 100% long equity and 25% short fixed income. It reflects these net weights in the exposures (100% equity, -25% fixed income).

If the portfolio added a further 25% short in Nvidia (NVDA, Equity) the portfolio would be 100% long and 50% short and display 75% net equity exposure and -25% net fixed income exposure.

In all other exposure exhibits, the data will presented as a net value relative to the gross value of the subcategory (namely, equity or fixed income).

For example, if a portfolio was 100% long the Financials Sector and 50% short the Healthcare sector, the gross exposure is 150%.

Financials exposure would be presented as 100% / 150% = 67%.

Healthcare exposure would be presented as -50% / 150% = -33%.

Custom Data Series

Custom Data Series (see here and here) lets you bring external data – such as private funds, real estate, cryptocurrency, and alternative investments – into Koyfin by uploading your own price and date series. With this feature, you can seamlessly integrate unsupported assets into Watchlists, Charts, and Portfolios, keeping everything in one place.

During creation of a Custom Data series, the Asset Allocation you define will appear in the asset allocation exposures of the model, and the data series will be including in holdings charts, tables, and performance and risk analytics.

Summary

Model portfolio exposures help investors manage risks and diversify by understanding investment distributions across asset classes, regions, sectors, and more. Holdings Contribution table provides detailed insights into the specific contributions of individual holdings to portfolio exposure. Use this tool to adjust your portfolio's weights with this tool to fine-tune exposure levels effectively.

Explore today and unlock the potential for smarter, more effective model portfolios!