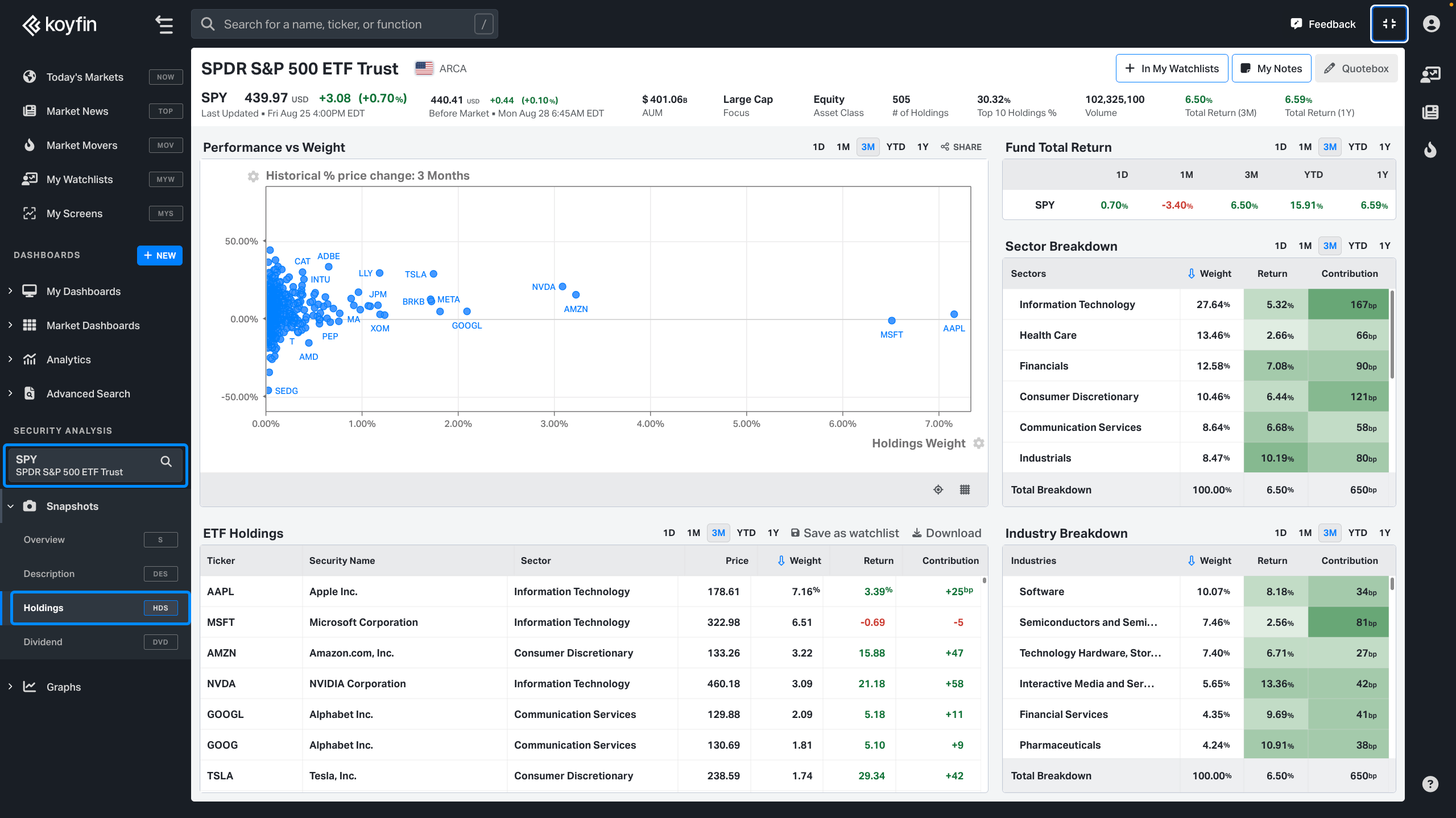

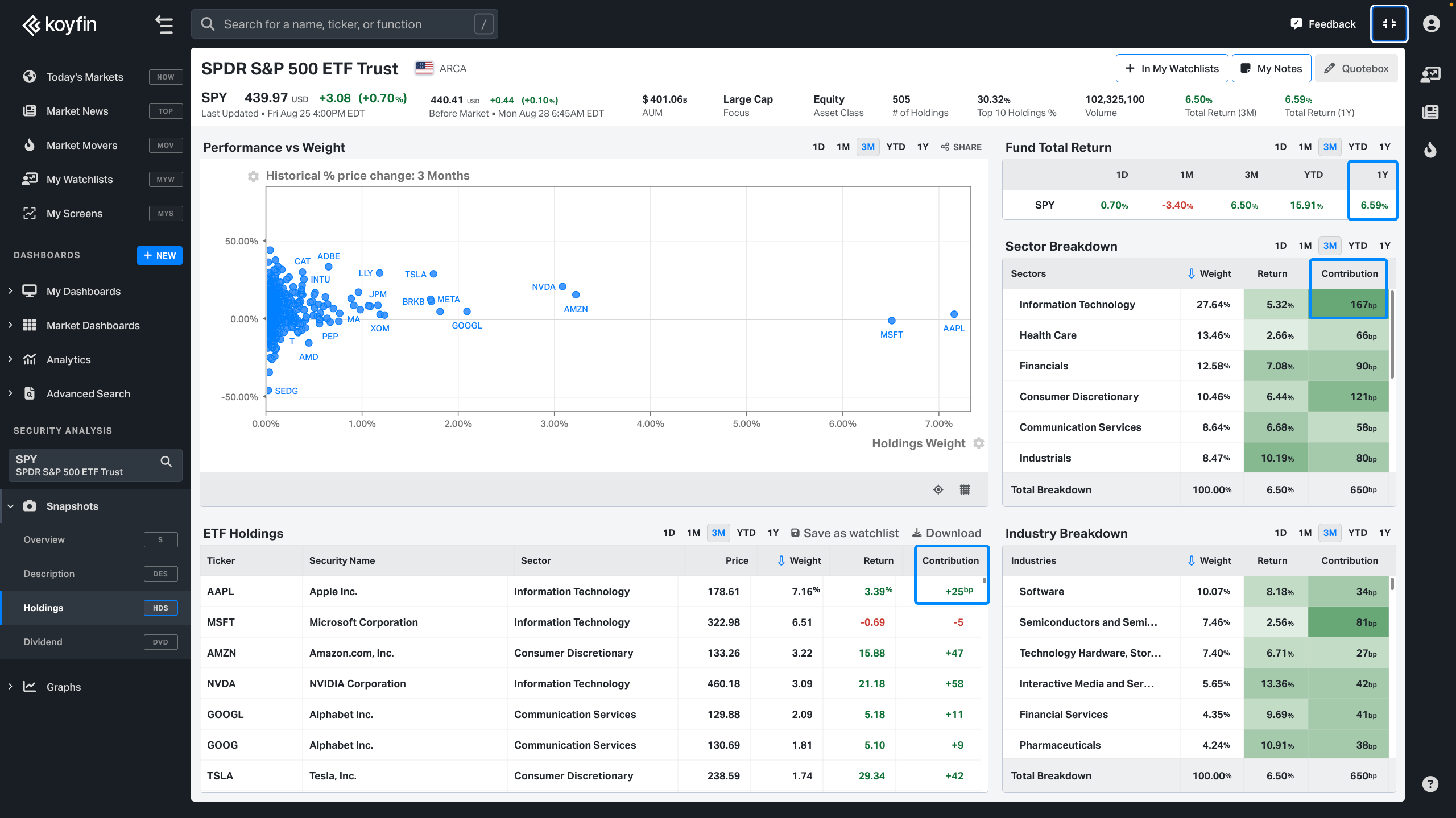

The ETF constituents and contribution function (HDS) provides an overview of the ETF composition and quantifies how components have contributed to the overall performance of an ETF. Each ETF stock member has a weight, performance and contribution. In addition, the HDS function breaks down the weight, performance and attribution by sector and sub-sector.

You can access the function when an ETF is loaded into Koyfin.

To access the function from the command bar, type <Ticker> and "HDS". For example, SPY HDS.

Contribution is a way to decompose the return of an ETF to explain how stocks and sectors have impacted the return of the ETF. The calculation for contribution is the performance multiplied by the weight. Contribution is additive, which means that summing up the contribution for individual components (stocks or sectors) is equal to the total performance of the ETF.

In the example below, the HDS function shows that the Dow Jones Industrials ETF (DIA) is up 10.5% over the past year. Information Technology sector accounts for 367 bps of the 10.5% 1-year return (about ⅓ of the return). And UnitedHealth Group Incorporated (UNH) accounts for 114 bps or about 10% (114 bps / 1050 bps) of the DIA 1-year return even though the stock is only 6.85% of the ETF.

Note: 1-day contribution is updated with live prices throughout the day.

Calculation details and caveats

For a stock, we calculate attribution by multiplying its estimated weight at the start of the period by its performance during the period. The weight is estimated because we lack historical constituent data and only have the current constituents. Additionally, we don’t account for stocks that were present at the beginning of the period but no longer exist due to acquisitions or delistings.

Ideally, the sum of stock and sector contributions would match the ETF’s performance. However, since we calculate contributions only for US-listed stocks and based on current constituents, the attribution doesn’t fully align with the actual performance. The “Unclassified” section acts as a balancing adjustment to reconcile our calculations with the ETF’s total return.