Whether you’re the Financial Advisors, Traders, Research Analysts and Sales, Koyfin has everything you need, all in one place.

Powerful insight for professional investors.

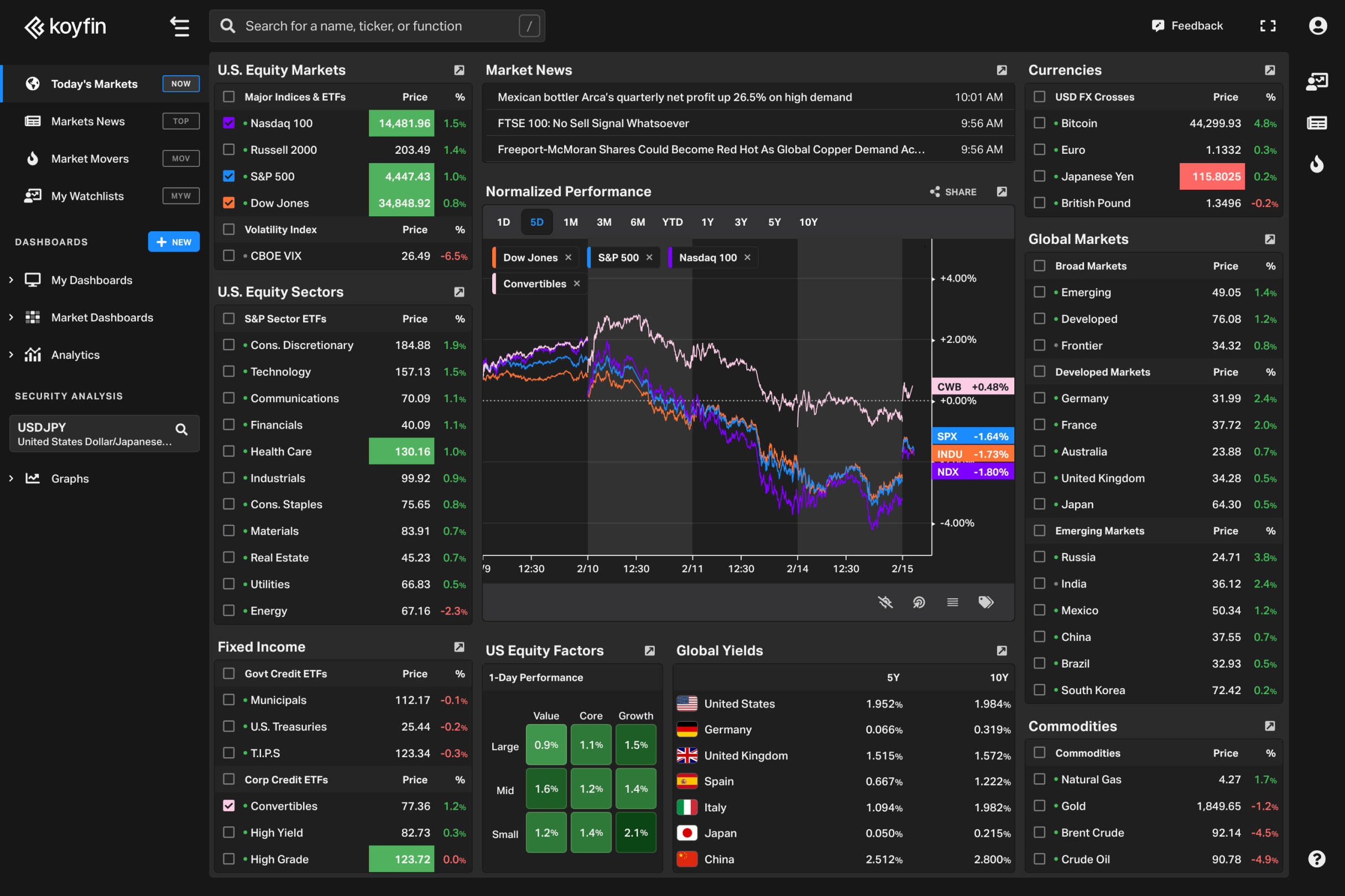

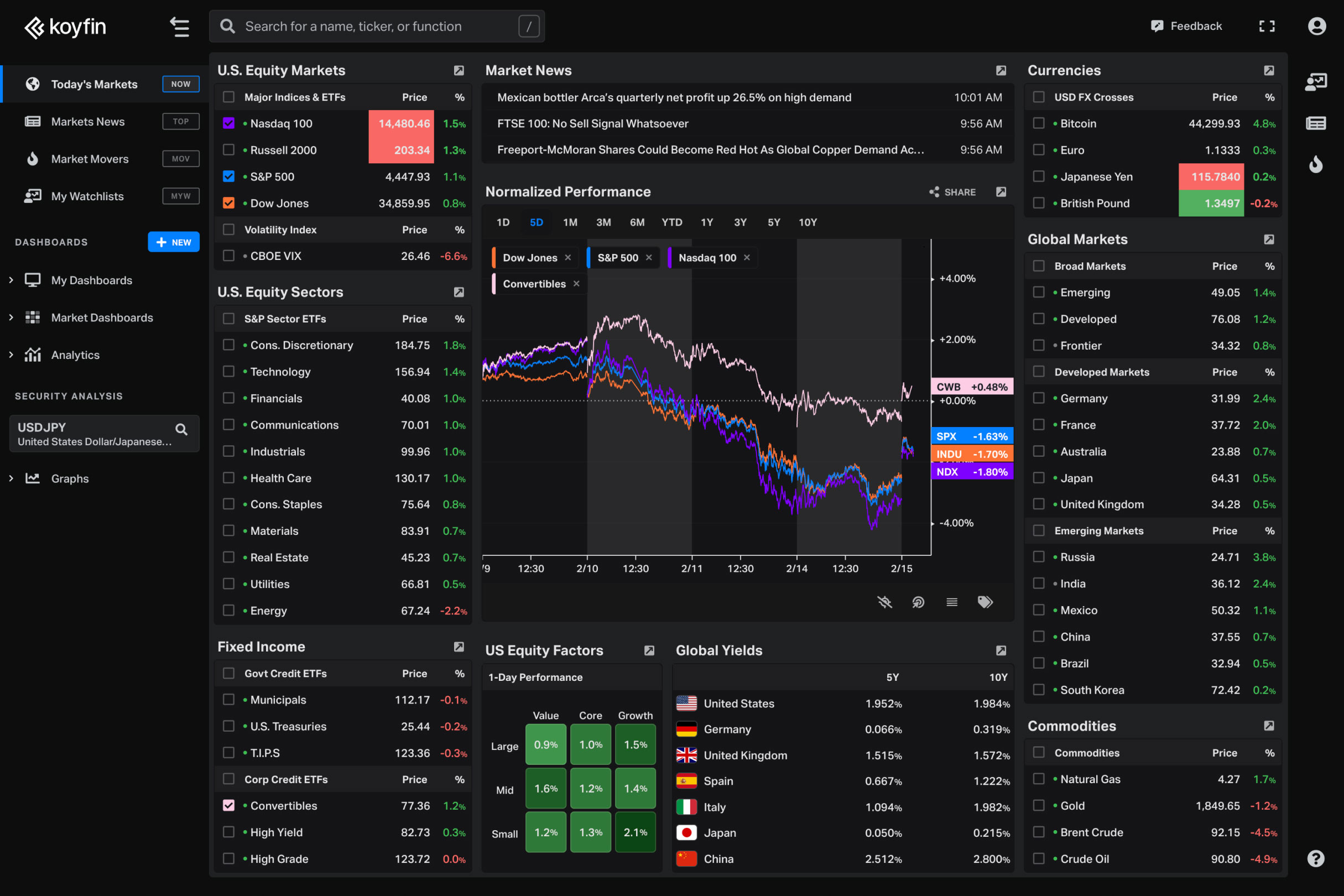

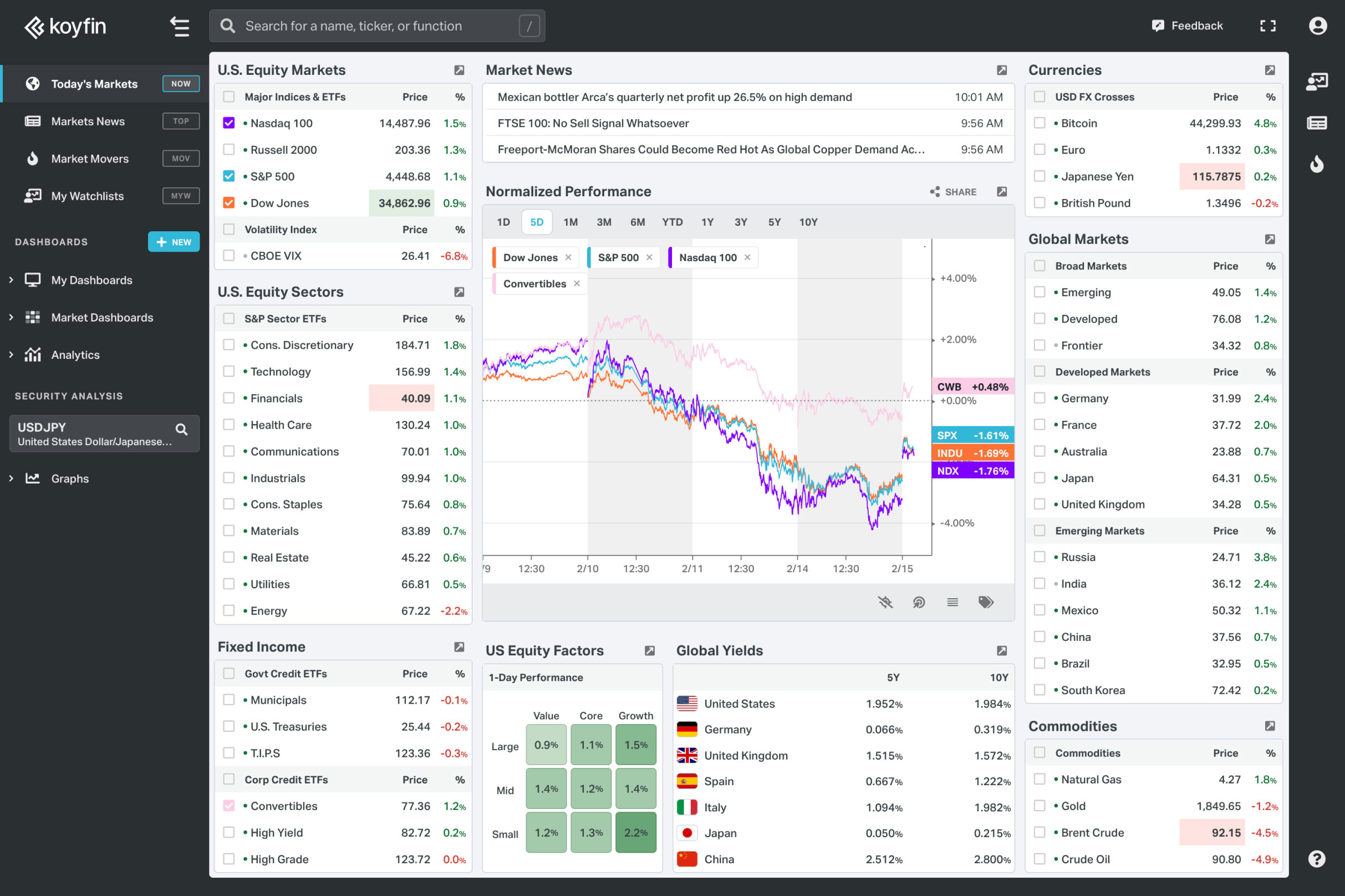

Live market data and powerful analytical tools that work the way you do.

Built by investors, for investors.

See more in less time

Our fully customizable platform puts you

in control. See the data you want to see, how you want to see it. Get instant access to live market data — from anywhere in the world.

Simplify your everyday

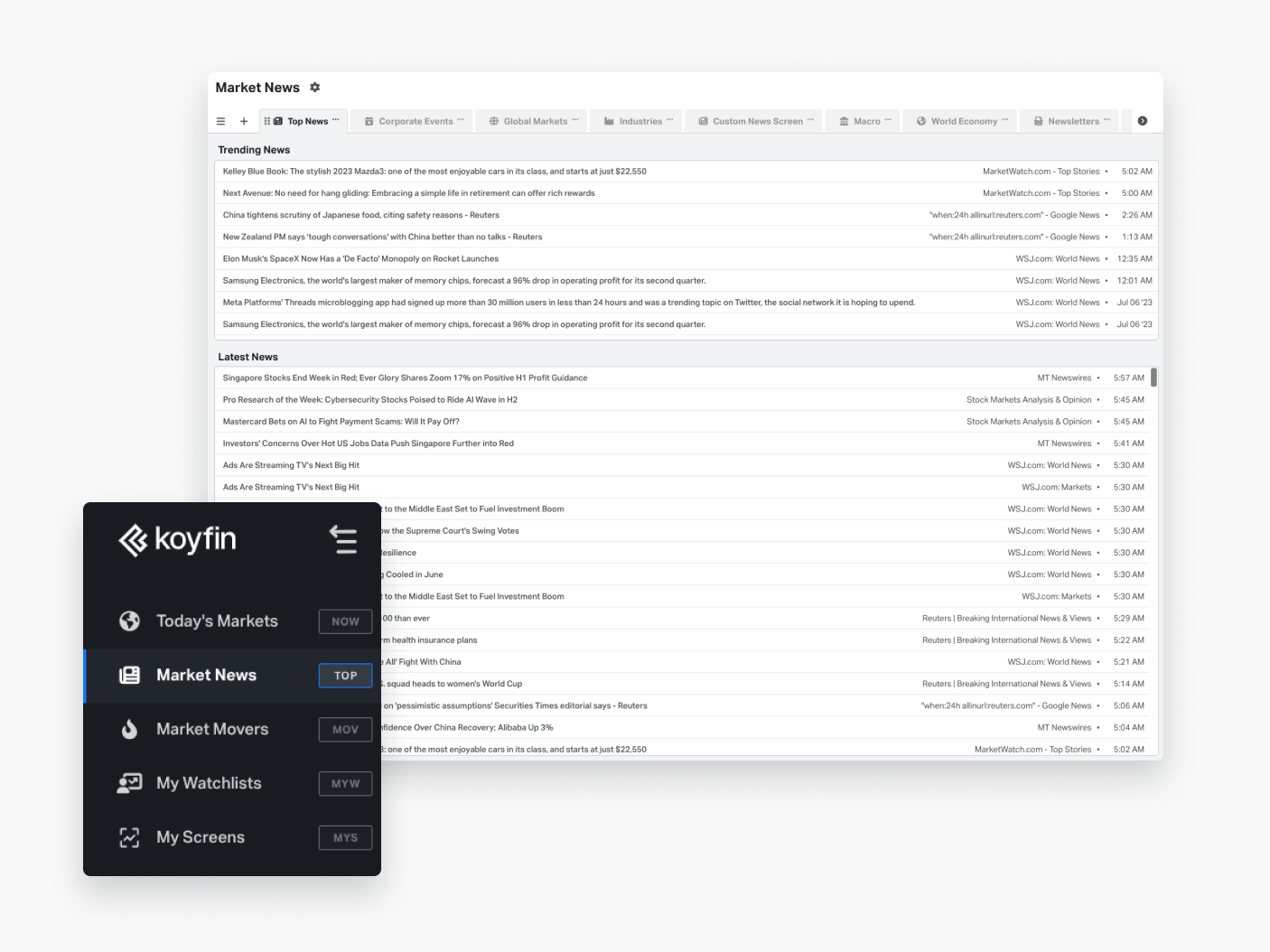

All the data you need in one place, a combined news and an easy to use interface make your working day brilliantly simple.

Designed to be different

We’re flexible. In a financial landscape full of conventional approaches, we break the mold to let you tailor your vision just the way you like.

Use Cases

A solution for every investor

We believe awesome data should be available to everyone, no matter the size of your portfolio. That’s why we have a price plan to suit everyone.

Discover how we

can help you

Professional Investors

Individual Investors

Macro Dashboards give you our best models for viewing bundled aspects of the financial landscape with just the right contextual detail. Explore and customize at will. Make our insight your own!

Students

Wherever you are on the stepping stones to your future, we’ve got the ideal platform. We respect what you’re doing, so we put your needs out in front.

Enterprise

Companies need to dissect markets. View commercial flows — or analyze competitors. Let Koyfin springboard your organization’s marketing and planning.

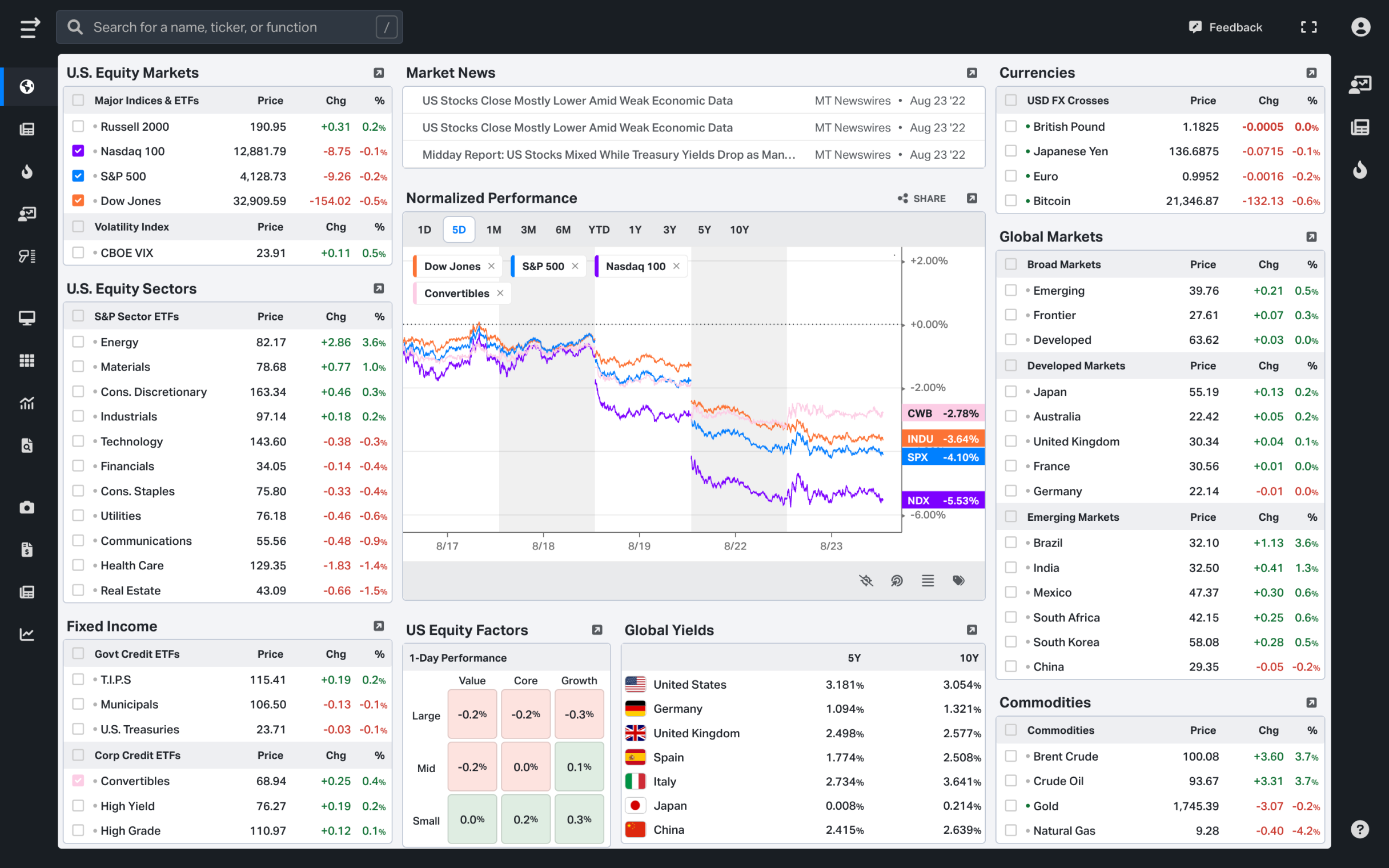

Data Coverage

Everything in

one place

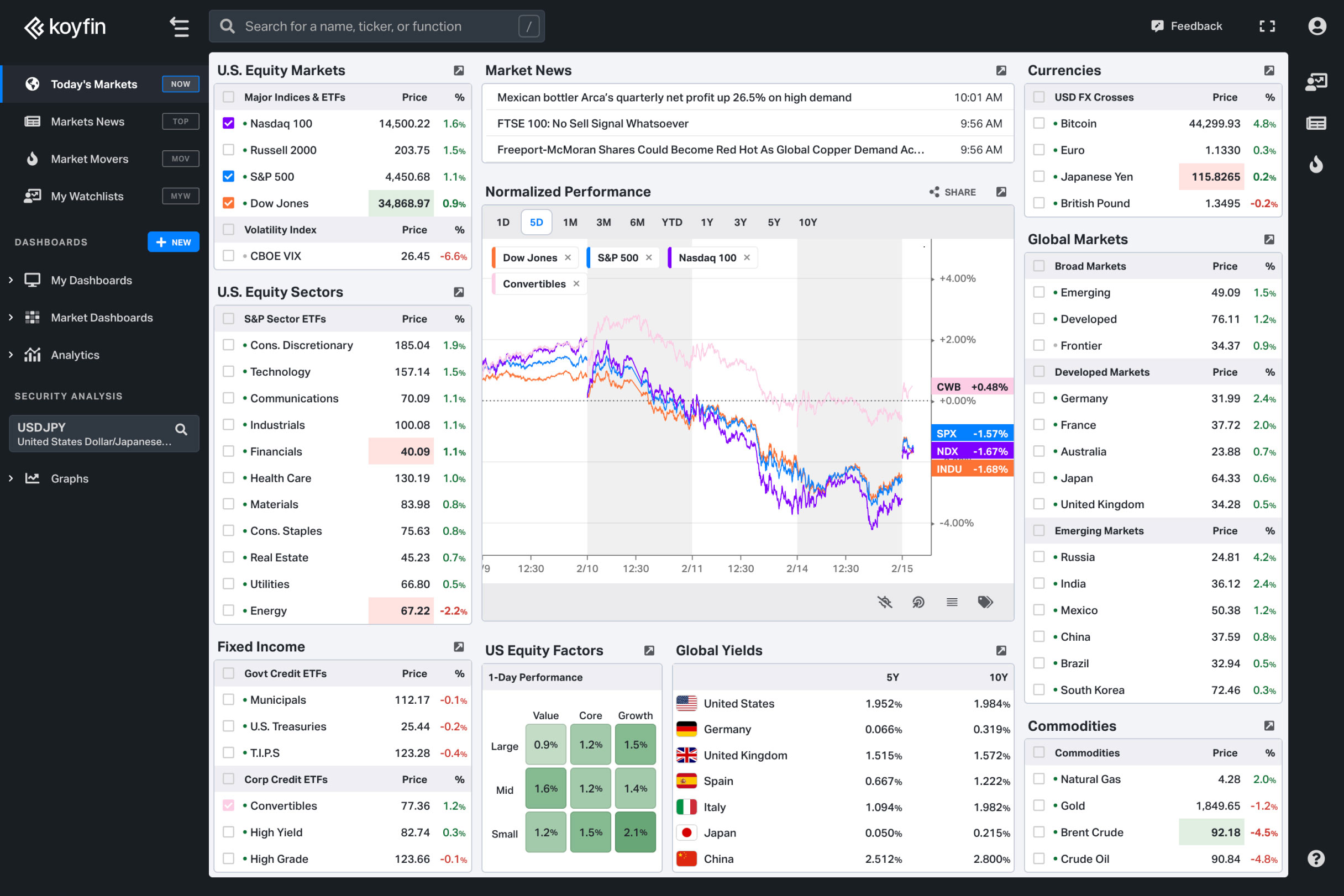

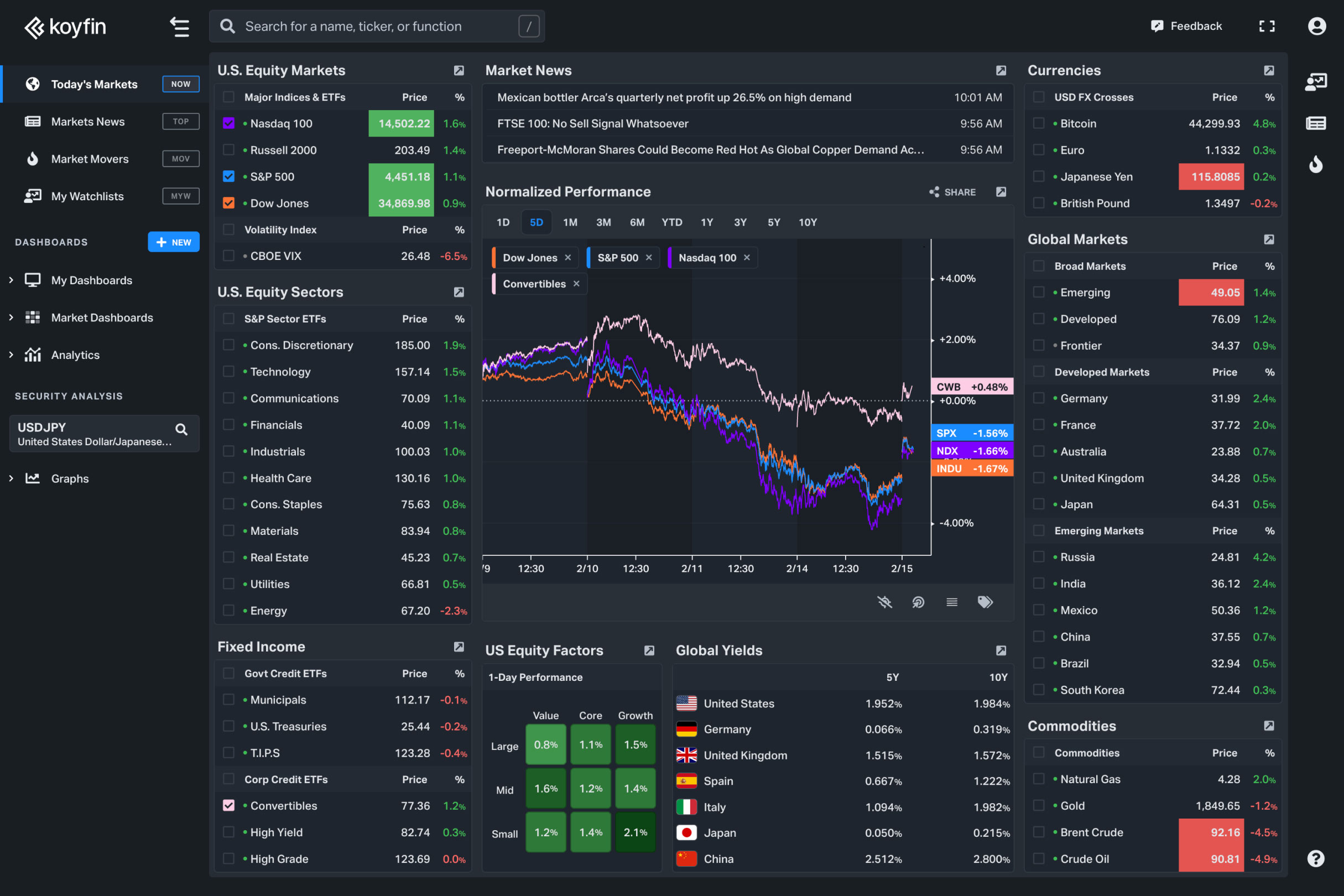

Koyfin is the only tool you need for a full picture of the financial markets. We’ve got your back. Our industry-leading data is right there for you, no matter the size of your portfolio.

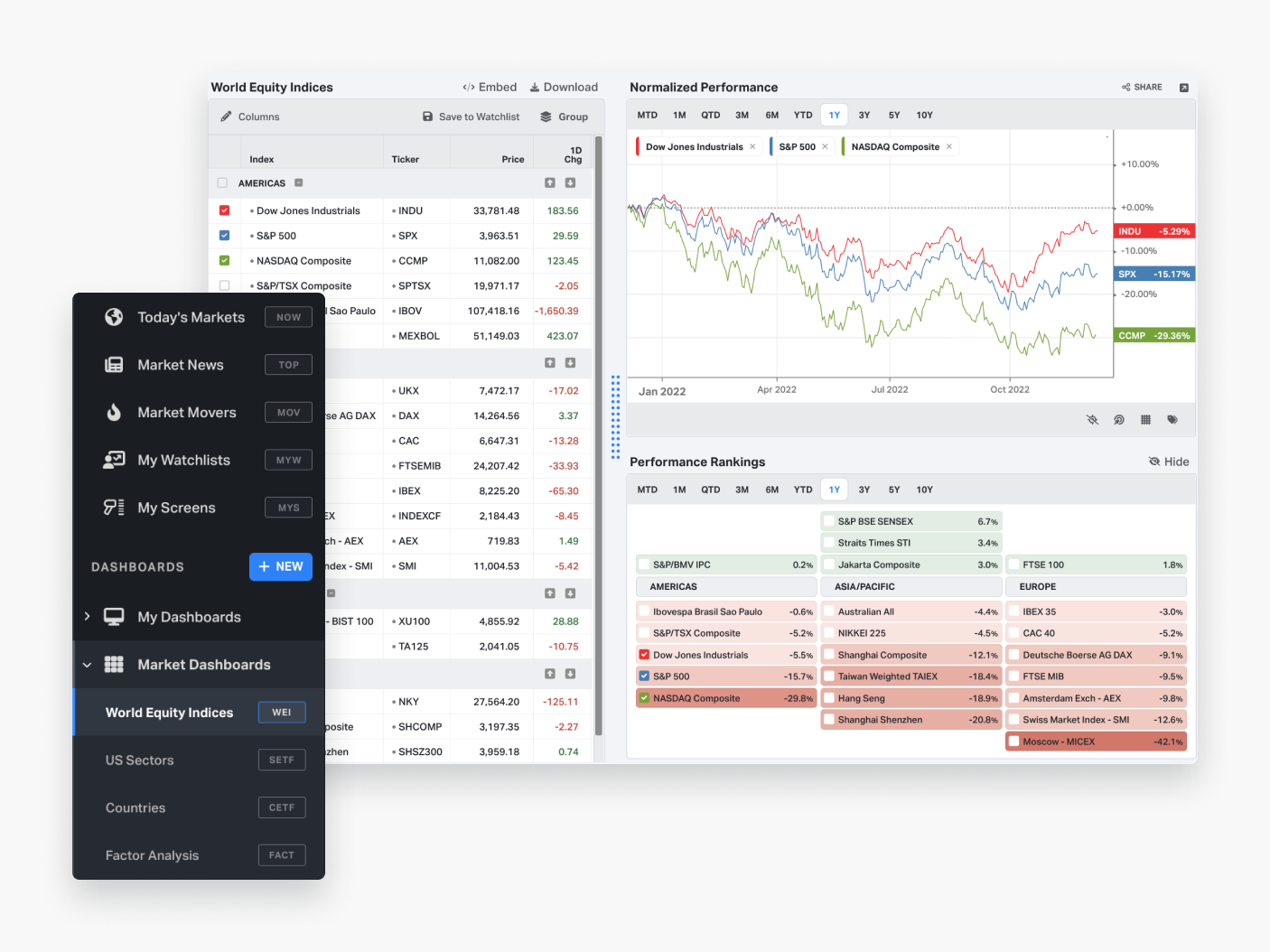

Stocks, the traditional mainstay of investing, sparkle with new excitement and insights under Koyfin’s adaptive analytical flair. Unleash new potential and profits with our deep-data views.

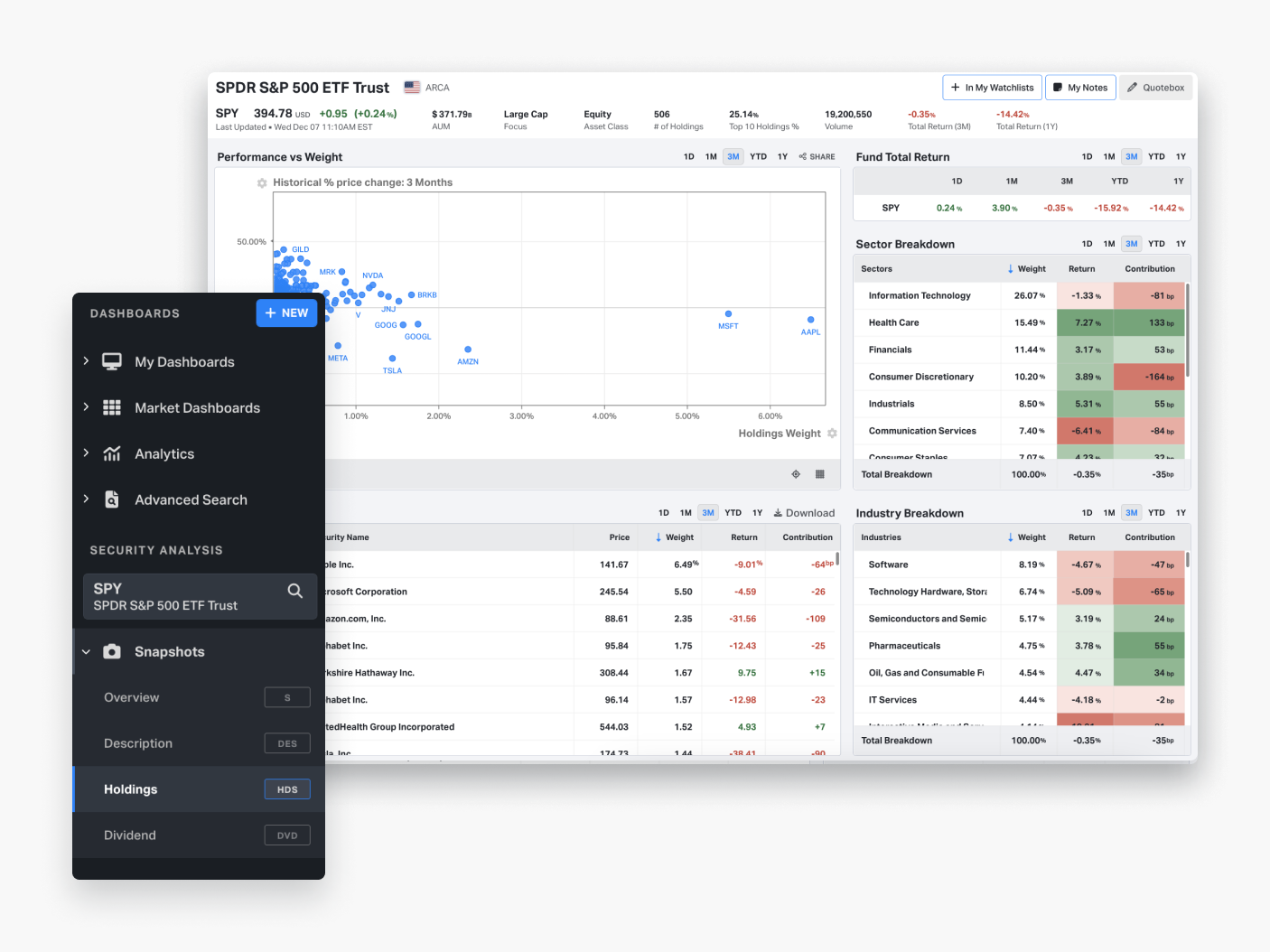

Exchange-traded funds let you mix and match an investment approach and scale in risk levels to suit your style, guarded or bold. Koyfin empowers you with tools to assess performance by constituent stock, sector and industry.

Koyfin knows mutual funds. They offer liquidity, built-in diversification, expert management, and more. Our custom search and filter options give you unrivaled insight. Make the leap to a winning portfolio.

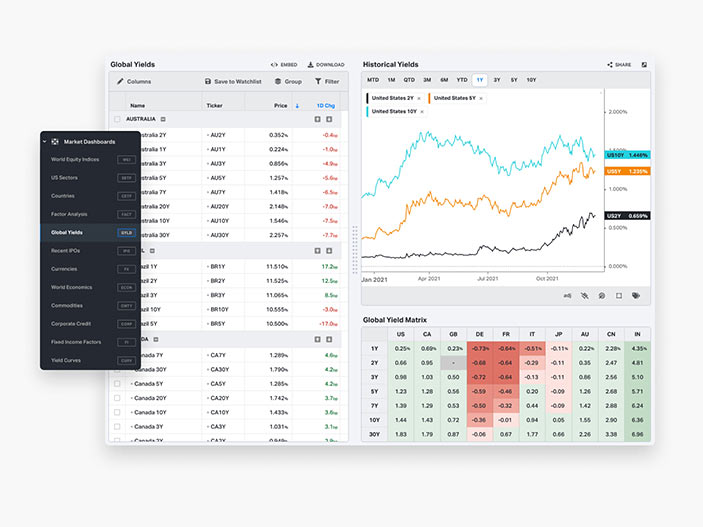

Global yields drive the price of every other asset class. Monitor live yields from 40 countries and analyze yield curve spreads historically. It’s all right here on Koyfin.

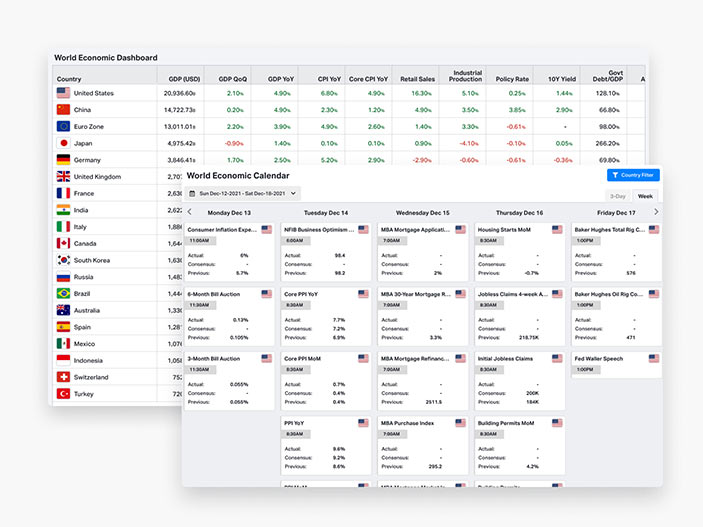

Tune in to the pulse of world markets and track what savvy investors track. We’ve got the tick of global economies, grouped by industry or sector, region, company size, and more.

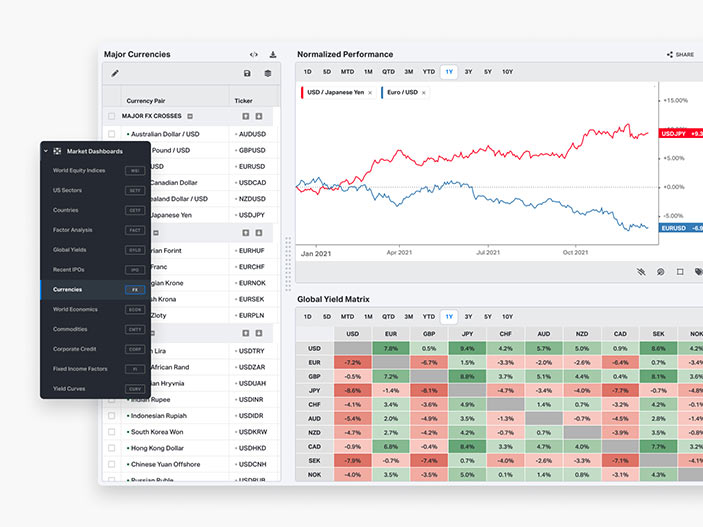

The world’s currencies trade billions of times a day — they’re the most liquid markets on the planet. Koyfin’s reenvisioned presentation of infinite data lets you see it all.

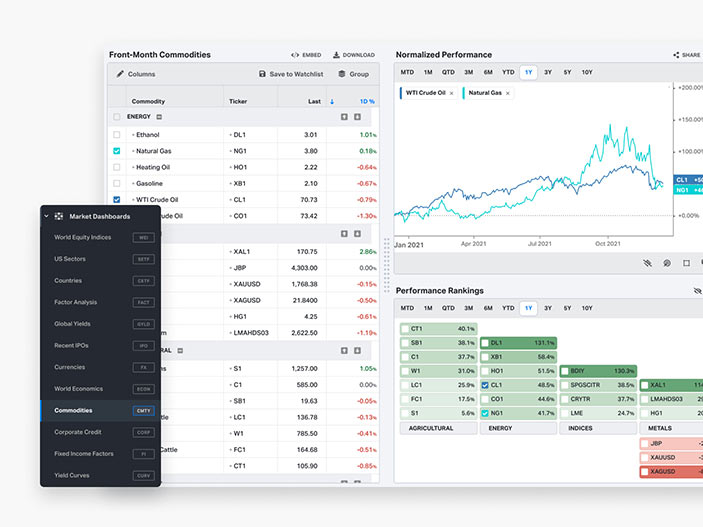

The basic goods of commerce can be your ideal trading vehicle. Beyond speculation, they shine as inflation hedges. Koyfin’s stellar charts let you balance your vision.

Your advantage extends past any international border, no visa required. Country trends are what’s tracking, so we make the world your oyster. Vital news and data, crunched the Koyfin way.

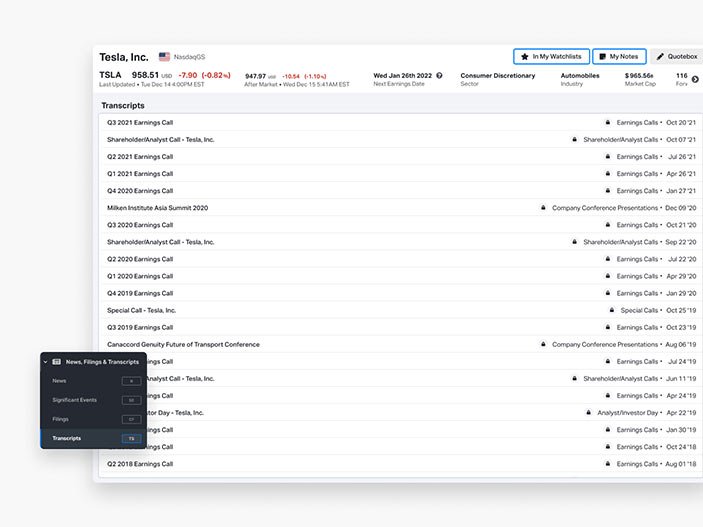

Stay vigilant with Koyfin’s power features. Transcripts let you review company events or evaluate critical sentiment from earnings calls. Search every company transcript for keywords in seconds. In a complex world, your leg up is seeing what others won’t.

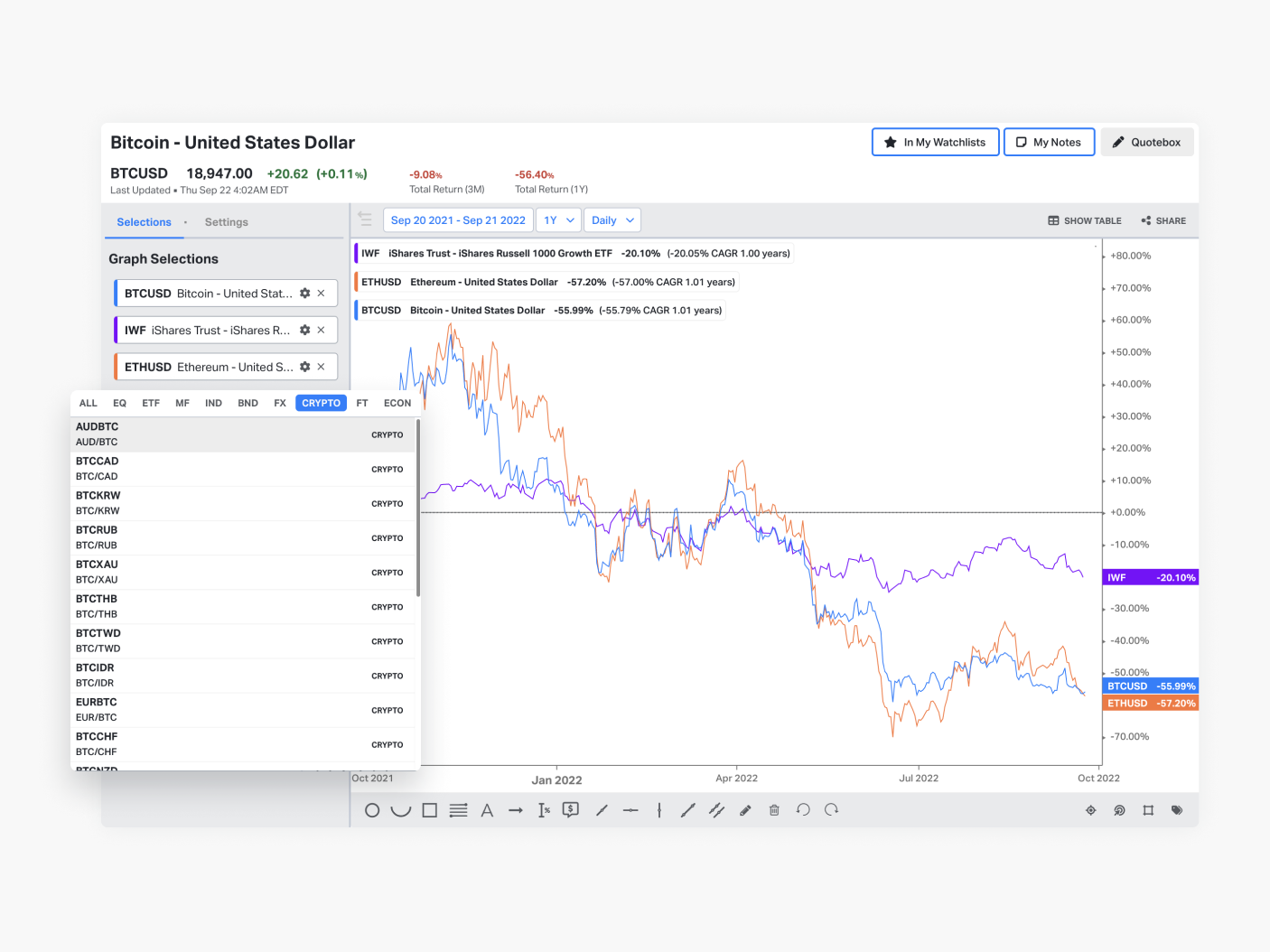

Whether you’re a seasoned trader or a Crypto newbie, Koyfin has you covered. Learn more, discover new technologies, and find the cryptocurrency data that fit your requirements.

Bring it home with relevant news for insight that matters most. Access trends and stories that shape and shake markets.

Our Mission

To equip every investor in the world, no matter their size, with the best data and tools; empowering them to achieve more.

Features

Featuring: infinite insight

Introducing Koyfin’s proprietary features, designed to make your life easier. You’ll see more data and gain insight. From powerful graphing tools to fully customizable dashboards, Koyfin puts you in control.

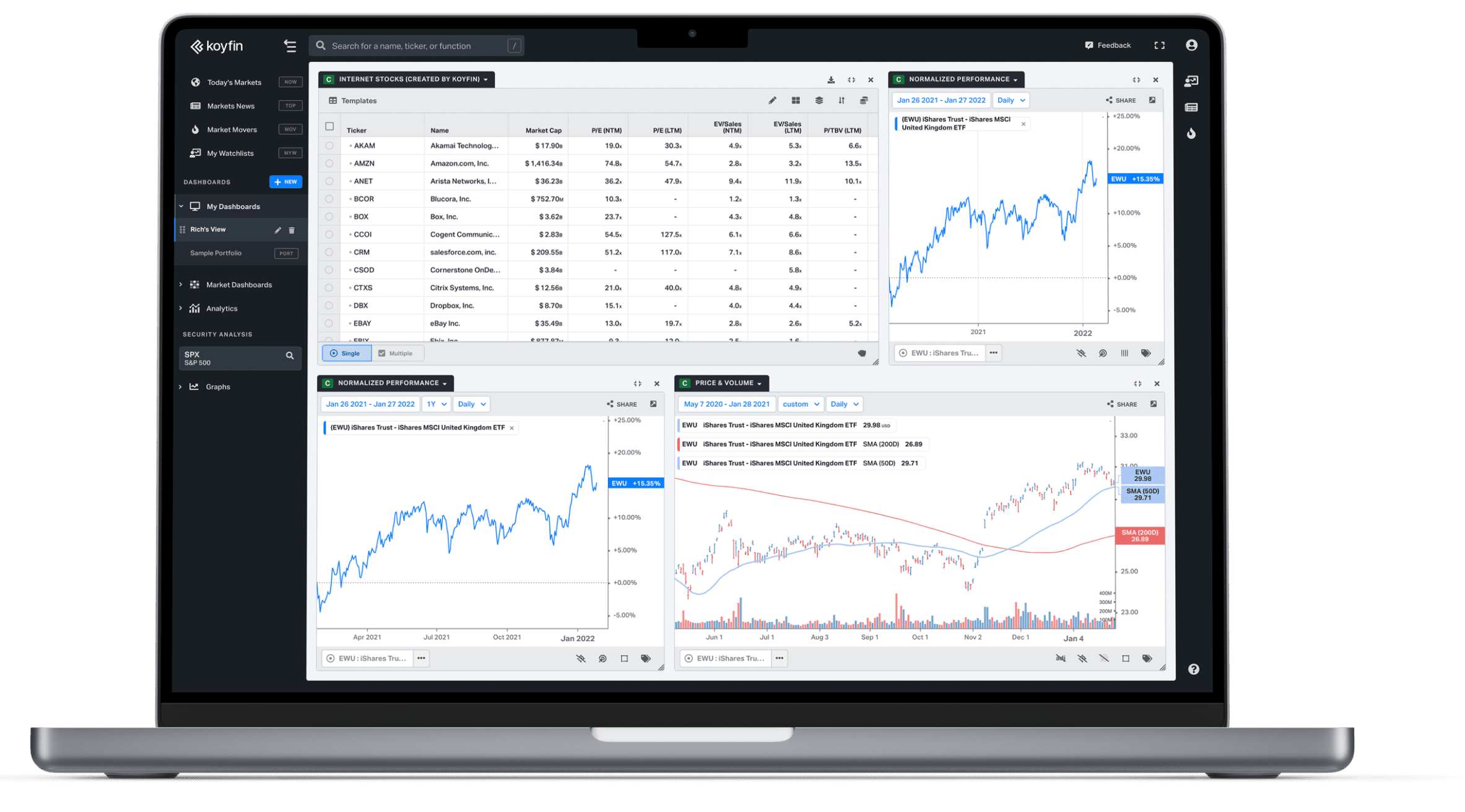

My dashboards

What’s your style? Build watchlists that come alive. Shape them to your style or needs. Custom dashboards let you perfect your vision. Focusing on the right data has never been easier.

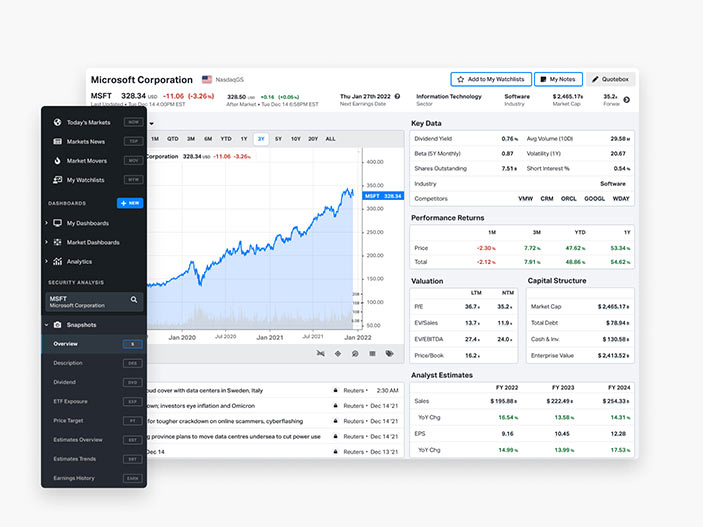

Financial analysis

The analysts speak, and the market moves. We help you keep up. Koyfin puts the world’s financial data at your fingertips. When the analysts speak, you can listen in.

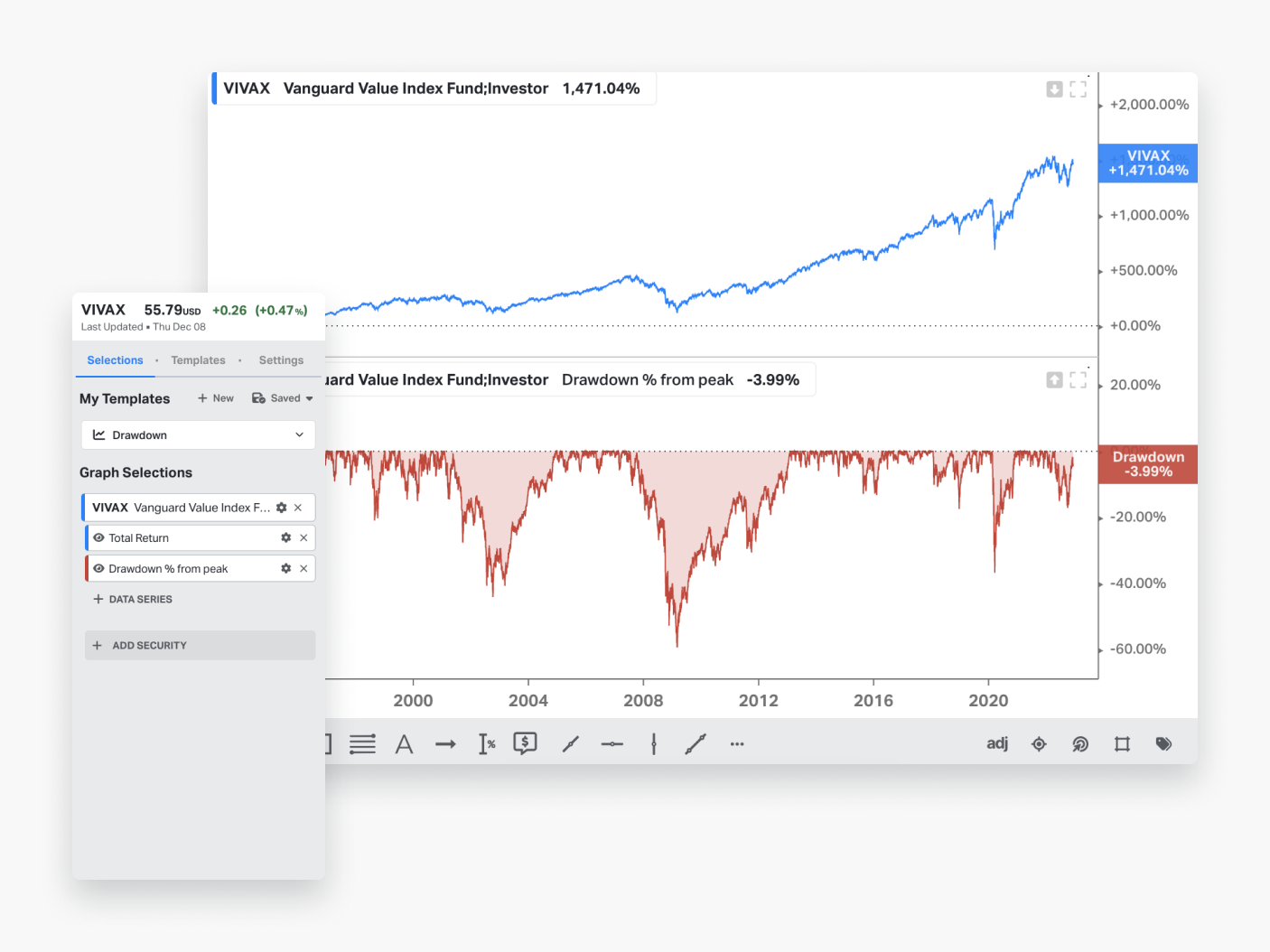

Advanced graphing

Humans love to visualize. Graphs drive today’s investing. Koyfin’s craft starts with fitting all the world’s data into radiant views. No more clunky interfaces! It’s the look and feel you wished for.

Equity Screener

Take control over the process of finding securities that drive the market. Our Equity Screener allows you to scan through over 100K global securities using 5,900+ filter criteria. Seize potential opportunities quickly and effectively!

Macro Dashboards

Macro Dashboards give you our best models for viewing bundled aspects of the financial landscape with just the right contextual detail. Explore and customize at will. Make our insight your own!

Customizable interface

Make it yours

Our interface is completely customizable — from the layout of your workspace to the color of your interface. Want to analyze a ticker? Just drag it out from the sidebar. Want to add a new element to your dashboard? Click once and it’s done.

Choose your theme

Beauty is only skin deep. Reskinning our platform is as easy as one, two, theme. Give it a try.

Puru Saxena

Independent Investor

Koyfin is an excellent research tool and with its global coverage of equities, analyst estimates and financials, it allows investors to carry out fast and comprehensive analysis. Koyfin is a great product!

Puru Saxena

Independent Investor

Jacob Radke

Capital Markets Analyst, Fjell Capital

Koyfin as a service is like no other. I’ve used Bloomberg terminals that my university provides but Koyfin’s service is perfect for what I need. It’s even comparable to the service that Bloomberg offers!

Jacob Radke

Capital Markets Analyst, Fjell Capital

Hal Peterson

Managing Principal, Mission Hill Advisors

I truly enjoy Koyfin. I have been in the investment advisory business for 35 years and although I subscribe to and use a number of tools ranging from Eikon to Zephyr, I open Koyfin every day.

Hal Peterson

Managing Principal, Mission Hill Advisors

Stephen Chen

A work-from-home investor, Singapore

Koyfin is one of the chief tools I use to get a quick overview of the markets, as it offers a great dashboard covering multiple asset classes across the globe. And because they also offer data and analysis on US-listed ETFs and funds.

Stephen Chen

A work-from-home investor, Singapore

Irnest Kaplan, CFA

Technology equity analyst and investor, Kaplan Equity Analysts

I have the hugest amount of respect for Rob and the Koyfin team. What these guys are doing is great – and they are empowering individual investors like me with tools that make it easier and faster to analyse companies all over the world!

Irnest Kaplan, CFA

Technology equity analyst and investor, Kaplan Equity Analysts

0 / 0

Great investments start with

great insight.

Join with the thousands of investors who’ve discovered Koyfin.